Let's be honest: traditional dental insurance can feel like a puzzle with half the pieces missing. For many of us here in San Diego, the high monthly premiums, confusing policies, and restrictive coverage just don't add up. It creates a frustrating gap between what you're paying for and the dental care you actually receive, which is why so many people are looking for better dental insurance alternatives.

Why Traditional Dental Insurance Falls Short

Ever get the feeling your dental insurance plan was designed to benefit the insurance company more than you? You're not alone. It’s a common story: you sign up for a policy expecting solid coverage, only to encounter a wall of limitations that leaves you paying a hefty out-of-pocket bill anyway.

This experience is incredibly common and gets right to the heart of the problem with the traditional insurance model. The entire system is often tangled in complexities that make getting affordable, quality care a real headache.

The Low Annual Maximum Dilemma

One of the biggest frustrations is the low annual maximum benefit. Most dental insurance plans will only cover around $1,500 to $2,000 per year. What's astonishing is that this figure hasn't really changed in decades, even as the cost of dental care has significantly increased.

Think about it: a single dental crown in San Diego can easily cost over $2,000. Your insurance might cover 50%, but once you hit that annual cap, the rest is your responsibility. If you need more than one major procedure in a year, you're almost guaranteed to be paying most of the bill yourself.

Common Frustrations with Insurance Plans

The annual cap is just the beginning. Patients frequently run into a host of other obstacles that make their plans feel like a poor value.

- Restrictive Waiting Periods: Worried about needing a major procedure soon? Many plans impose a six-month to one-year waiting period before covering significant work like crowns or root canals. This means you’re paying monthly premiums for benefits you can't even use yet.

- High Deductibles: Before your insurance contributes a single dollar, you must first pay a deductible. It's another out-of-pocket expense you have to cover before seeing any real benefit.

- Exclusions for Cosmetic Work: Thinking about veneers or professional teeth whitening to enhance your smile? Traditional insurance almost never covers procedures it deems "cosmetic," leaving you to pay 100% of the cost for any smile improvements.

- Confusing Paperwork and Claims: Wrestling with claim forms, pre-authorizations, and coverage denials can be a time-consuming and stressful administrative nightmare.

The core issue is a misalignment of interests. Insurance companies profit by minimizing payouts, while you and your dentist want to prioritize your oral health without financial barriers.

This is precisely why so many people are seeking dental insurance alternatives that offer more predictability and genuine value. Even employer-sponsored plans, which many people depend on, often cap annual benefits at just $1,000-$2,000. This leaves patients responsible for thousands in out-of-pocket costs for major work. This financial strain is what's truly fueling the shift toward other options, like in-house memberships that provide much clearer savings. You can explore more about these market trends and see what they mean for your wallet.

Exploring Your Top Dental Care Alternatives

If you're tired of the hoops traditional insurance makes you jump through, there's good news. A world of smarter, more direct alternatives exists. These options are designed to cut through the red tape and put you back in control of your healthcare spending, making quality dental care in sunny San Diego, where smiles are always on display, feel much more manageable.

Forget about navigating complex claims, deductibles, and waiting periods. These models are all about simplicity and direct value. Let's walk through the three most common paths for paying for your dental care without the usual insurance headaches. Each has unique perks, so you can find a fit that makes sense for you.

The Dental Discount Plan: A Costco Membership for Your Teeth

The easiest way to understand a dental discount plan is to think of it like a Costco or Sam's Club membership, but for your mouth. You pay a relatively small annual fee to join, and that membership unlocks access to a network of dentists who have agreed to provide their services at a significantly reduced rate.

It's a straightforward concept. You show your membership card at a participating San Diego dental office and receive an immediate discount—often between 15% and 50%—on nearly everything, from routine cleanings to major work like crowns and root canals.

Key benefits of dental discount plans include:

- No Waiting Periods: You can use your benefits the day you sign up. No waiting around for major services.

- No Annual Maximums: Unlike insurance, there's no cap on how much you can save in a year.

- Cosmetic Coverage: Many plans offer discounts on cosmetic procedures that insurance won't touch.

- No Claim Forms: The discount is applied right at the counter, so you never have to deal with paperwork.

This is a fantastic option for individuals or families who want to save money immediately and have access to a broad network of dentists without the complexity of an insurance policy.

The In-House Dental Membership: A Subscription for Your Smile

An in-house dental membership is perhaps the most direct and transparent alternative available. Think of it as a subscription service directly with your dentist's office. You pay a predictable monthly or annual fee to the practice, and in return, all your preventive care is completely covered.

This model creates a true partnership between you and your dental team. It shifts the focus from navigating a third-party payer's rules to simply getting the consistent care you need to stay healthy.

A typical in-house plan at a practice like Serena San Diego Dentist bundles all your essential preventive services—such as two cleanings, two exams, and all necessary X-rays—for the year. On top of that, your membership unlocks a set discount, usually around 10-20%, on any other treatments the practice offers, from fillings to veneers. Since these plans encourage regular visits, it's helpful to understand how often you should see a dentist to keep your smile healthy.

Why patients love in-house memberships:

- Simplicity and Transparency: You know exactly what you’re paying for and what you're getting. No confusing fine print.

- No Middleman: Everything is handled directly with the dental office, eliminating administrative hassle.

- Loyalty and Trust: It strengthens your relationship with a dentist you already know and trust.

- Predictable Budgeting: A flat fee covers your essential care, making it incredibly easy to budget for your dental health.

This is the perfect solution if you’ve found a San Diego dentist you love and want a simple, affordable way to manage your care without any surprises.

The Direct Pay Approach: Freedom and Flexibility

The simplest alternative is paying for services as you go, often called "paying out-of-pocket." This approach gives you ultimate freedom. You aren't tied to any network, policy, or membership fee. You can see any dentist you choose and simply pay for services when you receive them.

While it might sound like the most expensive route, paying directly can offer some negotiating power. Many dental practices provide a discount—often around 5%—for patients who pay in full at the time of service. This saves the office administrative costs associated with insurance, and they are often happy to pass those savings on to you.

This path works best for people who don't anticipate needing frequent dental work or who place a high value on the freedom to choose any provider without network restrictions. It's also a great way to handle one-off procedures when you don't want to commit to a year-long plan.

Comparing Dental Insurance Alternatives at a Glance

To make things even clearer, let's put these options side-by-side. Seeing the key differences laid out can help you quickly spot which approach aligns best with your budget and dental health needs.

| Feature | Traditional PPO Insurance | Dental Discount Plan | In-House Membership Plan |

|---|---|---|---|

| Payment Structure | Monthly Premium + Deductibles & Co-pays | Annual or Monthly Membership Fee | Annual or Monthly Membership Fee |

| Waiting Periods | Yes, typically for major services | No, benefits are immediate | No, benefits are immediate |

| Annual Maximums | Yes, usually a yearly limit on coverage | No, unlimited savings potential | No, discounts are unlimited |

| Network | Must use "in-network" dentists for full benefits | Must use participating network dentists | Limited to one specific dental practice |

| Paperwork | Yes, claims, pre-authorizations, etc. | No, discount applied at time of service | No, benefits managed by the practice |

| Cosmetic Coverage | Almost never covered | Often includes discounts | Often includes discounts |

Ultimately, the best choice boils down to your personal circumstances. If you value flexibility and a wide network, a discount plan might be the answer. If you've found a dentist you love and want a simple, predictable budget, an in-house plan from a clinic like Serena San Diego Dentist is hard to beat.

How In-House Dental Memberships Work

What if you could receive excellent dental care without ever dealing with an insurance company? That’s the simple, powerful idea behind an in-house dental membership. Think of it as a direct partnership with a dental practice you already know and trust, created to make top-tier care both predictable and affordable.

It really is as simple as it sounds. The whole system works like a subscription service for your smile. You pay a consistent, easy-to-budget fee straight to your dentist's office, usually monthly or once a year. In return, all your essential preventive care is completely covered.

This straightforward exchange cuts out the complexity and red tape of traditional insurance, giving you a clear, stress-free path to great oral health.

What Your Membership Typically Includes

At their core, in-house memberships are designed to do one thing very well: encourage you to get consistent preventive care. After all, that’s the foundation of long-term dental health. While the specifics can vary between practices, a solid plan like the one at Serena San Diego Dentist will almost always cover the essentials:

- All Routine Preventive Care: This means your regular cleanings, comprehensive exams, and any necessary X-rays for the year are 100% covered.

- Significant Discounts on Other Treatments: If you need anything extra—from fillings and crowns to cosmetic work like veneers—you get a set discount, often between 10-20%.

- No Hidden Fees or Surprises: The costs are laid out clearly from day one, ensuring you can plan your budget effectively.

With a structure like this, you never have to postpone a check-up because of cost. It’s all about catching small issues before they become bigger, more expensive problems.

The Game-Changing Advantages

The true magic of an in-house membership becomes clear when you compare it to a traditional insurance policy. The benefits go far beyond just covering your cleanings.

An in-house plan fundamentally changes the relationship you have with your dental care. It shifts the focus from navigating coverage rules to proactively managing your health with a trusted partner like Dr. Serena.

Here are the key advantages that our San Diego patients truly appreciate:

- Zero Deductibles: You never have to pay a certain amount out-of-pocket before your benefits kick in.

- No Annual Maximums: There’s no ceiling on how much you can save. If you need extensive work done, your discount applies to all of it.

- No Waiting Periods: Your benefits are active the moment you sign up, so you can book that needed appointment right away.

- No Claim Forms or Hassles: Since the agreement is directly between you and your dentist, all that administrative pain disappears.

This no-nonsense system is a breath of fresh air for anyone who has ever been frustrated by insurance paperwork and denied claims. For those curious about the backend, practices often use membership management software platforms to keep everything running smoothly.

Why This Model is a Perfect Fit for San Diego

Here’s a startling fact: in the U.S., a staggering 40% of adults have untreated tooth decay, often due to inadequate or non-existent insurance coverage. This has created a huge demand for better dental insurance alternatives. Practices like ours at Serena San Diego Dentist are stepping up to meet that need with in-house plans that ensure preventive care is always covered and offer real discounts on other treatments for one predictable fee.

If you’re someone who values building a strong, lasting relationship with your healthcare provider, this model is a fantastic fit. It fosters trust and ensures the most important decisions about your health are made by you and your dentist—not by an insurance agent hundreds of miles away. Still exploring your options? Our guide on how to choose the right dentist in San Diego offers some great insights for finding a practice that truly fits your needs.

Making Your Dream Smile Financially Possible

Let's be realistic: even the best dental savings plans may not cover the entire cost of a major smile transformation. When you're considering significant cosmetic work like veneers, a full set of implants, or a complete smile makeover in San Diego, the initial price tag can feel daunting. But this is precisely where smart financial planning comes in.

A lack of traditional insurance should never stand between you and life-changing dental care. At Serena San Diego Dentist, we offer several excellent ways to break down larger costs into payments that fit your budget, so you can move forward with treatment without the stress.

Third-Party Financing: The Healthcare Credit Card

One of the most popular ways patients manage the cost of major dental work is through specialized third-party financing companies. You can think of them as credit cards designed specifically for medical and dental procedures.

CareCredit and LendingClub are two of the biggest names in this space. The process is surprisingly simple:

- You fill out a quick application, which can often be done right here in our San Diego office.

- You typically receive an approval decision in just a few minutes.

- Once approved, you can use the funds to pay for your treatment immediately.

The real game-changer is their promotional financing. Many plans offer 0% interest if you pay off the balance within a set period, like 6, 12, or even 24 months. This allows you to get the care you need right away while spreading the payments over time, all without paying a dime in interest. For dental practices, offering these flexible options relies on sophisticated backend systems, including specialized medical billing software to keep patient accounts and payments running smoothly.

Using Tax-Advantaged Funds: HSAs and FSAs

Don't overlook the power of tax-advantaged savings accounts. If your employer offers a Health Savings Account (HSA) or a Flexible Spending Account (FSA), you can use that pre-tax money to cover your dental care.

Using an HSA or FSA is like getting an automatic discount on your dental work. Because you're paying with money that hasn't been taxed, you effectively lower the total cost of your treatment by your tax bracket percentage.

Here’s a quick breakdown of how these accounts can help you pay for that new smile:

- Health Savings Account (HSA): If you have a high-deductible health plan, you may have an HSA. The great thing about HSAs is that the money you save is yours to keep and it rolls over year after year, making it perfect for planning larger procedures.

- Flexible Spending Account (FSA): With an FSA, you set aside pre-tax money specifically for healthcare costs each year. These are typically "use it or lose it" accounts, so they're ideal for treatments you already have on the calendar.

By getting creative, you can combine these tools to build a smart, affordable path to the smile you’ve always wanted. For example, you could use a CareCredit plan for the initial payment and then use your HSA funds to pay it off comfortably over time. Ready to enhance your smile? Schedule a free consultation at Serena San Diego Dentist today!

How To Choose The Right Dental Plan For You

Now that we’ve unpacked the different alternatives to traditional insurance, it’s time to determine which one makes the most sense for you. There’s no single "best" option—the right choice truly comes down to your personal situation.

By taking a few minutes to think through your needs, your budget, and your relationship with your dentist, you can confidently pick a path that works for your smile and your wallet. Let's walk through the process.

Assess Your Dental Needs And Goals

First, be honest about the state of your oral health and what you're looking to achieve. Are you just trying to keep up with routine maintenance, or are you planning for a major dental project?

This is the most critical question to ask yourself.

- For Primarily Preventive Care: If your teeth are generally healthy and you just need to cover your twice-yearly cleanings, exams, and maybe an occasional filling, an in-house membership plan is almost always the most straightforward and cost-effective route. You get predictable costs for the services you know you'll use.

- For Major Restorative or Cosmetic Work: If your plans include crowns, implants, or veneers, your priorities shift. The goal here is to find the greatest possible savings on these more expensive treatments. An in-house plan is still a fantastic option, but it's also worth comparing it with a dental discount plan to see which one offers a better percentage off major procedures.

Evaluate Your Budget And Payment Preferences

Next is your financial comfort zone. How do you prefer to handle healthcare costs? Thinking about this will help you avoid financial stress and ensure you can always get the care you need.

The right financial tool isn't just about saving money; it's about providing peace of mind. Choosing a plan that aligns with your budget prevents financial stress from becoming a barrier to essential care.

Some people love the predictability of a fixed monthly or annual fee, which makes budgeting simple. If that's you, an in-house membership fits perfectly. Others prefer to pay for services only when they need them, avoiding recurring charges. In that case, a direct-pay or financing approach might feel more comfortable.

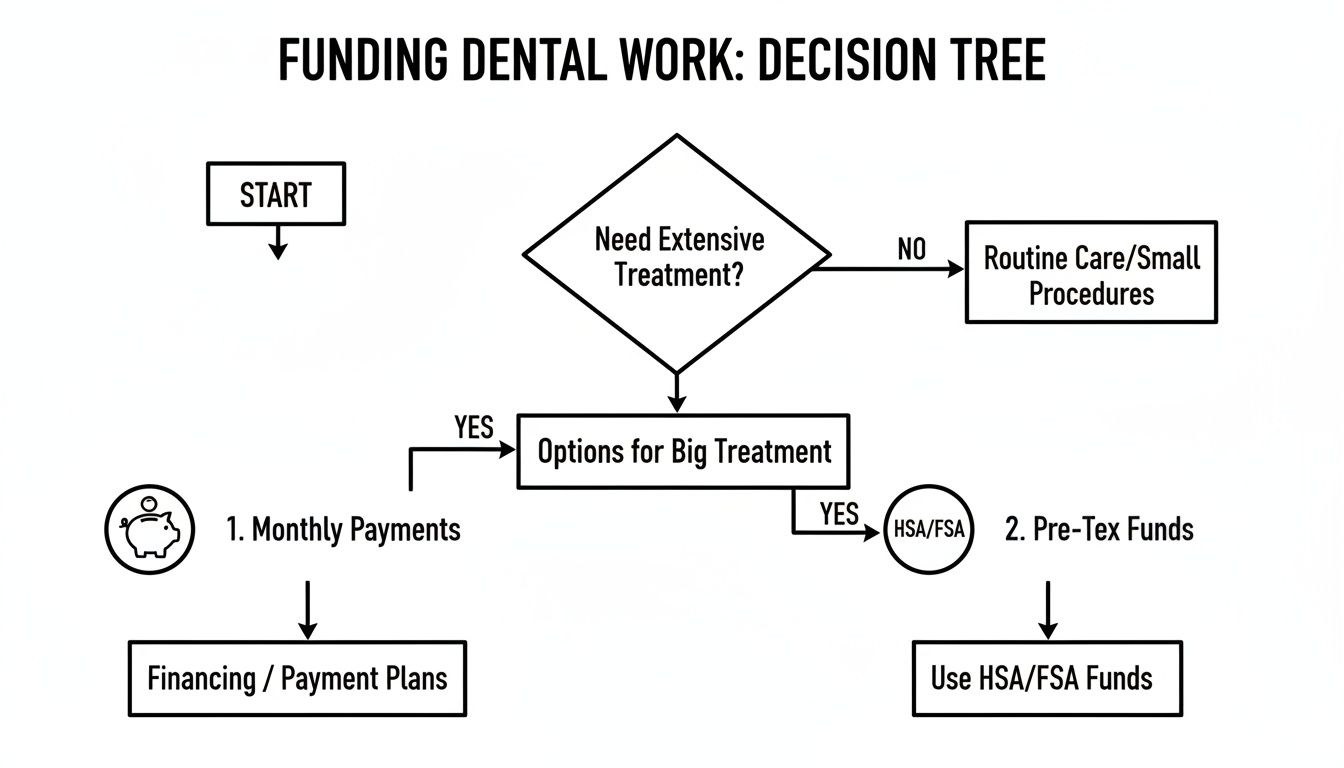

This decision tree gives you a great visual for how to think about funding more extensive dental work.

As you can see, when facing a larger treatment cost, you have clear paths to make it manageable, whether that’s breaking it into monthly payments or using dedicated health savings.

Consider Your Dentist Relationship

Finally, ask yourself how important it is to stick with a specific dentist. Do you value the relationship you have with your current dental team, or do you prefer the flexibility to choose from a broad network?

If you already have a dentist in San Diego you know and trust—like our team here at Serena San Diego Dentist—an in-house membership is a no-brainer. It's designed specifically for our patients and ensures you continue receiving care from the people who know your history. You can learn more about how our practice handles dental insurance and payment options on our site.

On the other hand, if you don't have a regular dentist or you like having a long list of providers to choose from, a dental discount plan might be a better match. These plans provide a network of participating dentists, giving you more options even if it means a less personal connection.

Which Dental Care Option Is Best For You?

Still trying to decide? This table breaks it down based on common scenarios to help you see which alternative might be the best fit for your life right now.

| Your Situation | Best Fit Alternative | Why It Works |

|---|---|---|

| "My teeth are healthy. I just need my cleanings, checkups, and maybe a small filling." | In-House Membership Plan | It offers the best value for routine preventive care with no deductibles or annual maximums. |

| "I need a crown and a few other significant procedures in the next year." | In-House or Discount Plan | Compare the discounts. The in-house plan is simpler, but a discount plan might offer a higher percentage off. |

| "I hate surprise bills. I want to know exactly what I'll pay each year." | In-House Membership Plan | Provides a predictable, subscription-style cost for all your basic preventive needs. |

| "I don't have a regular dentist and want the freedom to choose from a list." | Dental Discount Plan | These plans are built around a network of providers, giving you flexibility and choice. |

| "I rarely go to the dentist but I have a chipped tooth that needs fixing ASAP." | Third-Party Financing | Allows you to get the care you need immediately and pay for the one-time expense in installments. |

By weighing these three key factors—your dental needs, your budget, and your dentist preference—you can confidently choose the dental plan that will support your oral health for years to come.

Common Questions About Dental Insurance Alternatives

When you begin exploring alternatives to traditional dental insurance, a few questions always arise. It's a different way of thinking about paying for your care, so it's completely normal to want the details straight. We've compiled the most common questions our San Diego patients ask to give you clear, honest answers and help you feel confident in your choice.

Are Dental Discount Plans The Same As Insurance?

Not at all—they function in completely different ways, and it’s a crucial distinction to understand.

Think of it this way: insurance is a safety net you pay for monthly. You pay a premium, and an insurance company agrees to share the financial risk with you. They will cover a portion of your dental bills, but only after you’ve paid a deductible and as long as you stay under your annual spending cap.

A dental discount plan is more like a membership club for your teeth. You pay a flat annual fee to join and get instant access to a network of dentists who offer their services at a pre-negotiated, lower rate. There are no claim forms to file, no waiting for approvals, and no annual limits on how much you can save.

Can I Use An In-House Membership For Cosmetic Dentistry?

Yes! And this is honestly one of the biggest advantages of an in-house plan. For anyone interested in improving the appearance of their smile, this is where these plans truly shine.

Traditional insurance almost never covers procedures it considers "cosmetic," like porcelain veneers or professional teeth whitening. They simply won't pay, leaving you to cover the entire cost yourself.

In-house membership plans, on the other hand, are designed to make all of a practice's services more affordable. This usually means your membership gets you a set discount (often 10-20%) on everything the dentist offers, including those amazing cosmetic and restorative treatments. It brings your dream smile that much closer to reality.

Is Paying With Cash Cheaper Than Using A Plan?

For anything beyond a simple cleaning, a structured plan almost always saves you more money. It might seem like paying cash upfront would be the most direct and cheapest way, but the numbers usually tell a different story.

Some dental offices might offer a small "pay-in-full" discount, perhaps 5%, if you pay with cash on the day of your service. It saves them some administrative hassle, and they pass a little of that savings on to you.

However, a formal in-house membership or a quality dental discount plan offers much larger, contractually guaranteed savings. The discounts from a dedicated plan will easily beat the small break you might get for paying in cash, especially for more involved treatments.

Can I Combine A Dental Plan With My HSA Or FSA Account?

Absolutely—and this is a very smart way to stack your savings. You can definitely use the funds in your Health Savings Account (HSA) or Flexible Spending Account (FSA) to pay for your dental work.

Here’s how you can make it work for you:

- First, your in-house membership or discount plan lowers the total cost of your treatment.

- Then, you use your pre-tax HSA or FSA dollars to pay for the remaining, discounted balance.

It's a powerful one-two punch for saving money. You get the plan discount first, then you pay the rest with tax-free funds. That's like getting a second discount equal to your tax rate.

Just keep in mind that while you can use these funds for your dental treatments, the annual fee for the membership plan itself is usually not an eligible expense. It's always a good idea to double-check the rules with your HSA or FSA administrator.

Ready to explore a simpler, more affordable way to get the dental care you deserve? At Serena San Diego Dentist, we offer a straightforward in-house membership plan designed to cover your preventive care and provide significant savings on all other treatments. Visit us online to learn more and take the first step toward a healthier, more confident smile.