Trying to find the right dental insurance in San Diego can feel like piecing together a complicated puzzle, but getting it right is the secret to unlocking affordable, high-quality dental care. A great plan strikes the perfect balance between your monthly premium and the coverage you get, so routine check-ups and major procedures don't break the bank. For most San Diegans, the choice boils down to a flexible PPO plan or a cost-effective DHMO.

Navigating Your Dental Insurance Options in San Diego

Let's be honest: staring at a long list of dental insurance plans can be overwhelming. Maybe you're trying to figure out how to afford a crown you know you need, or you just want to make sure your family's six-month cleanings are covered without surprise bills. This guide is here to cut through the confusion and give you a clear roadmap for understanding your options right here in America's Finest City.

My goal is to help you feel confident picking a plan that protects both your smile and your wallet. We'll start by breaking down the two main paths you can take—PPO and DHMO plans—and use simple analogies to show you how each one works. Think of this as your personal guide to balancing costs, choosing the right dentist, and knowing exactly what you're paying for.

Why Your Choice Matters

Picking the right dental insurance isn't just about saving money. It's about ensuring you can get the care you need, right when you need it. A plan that fits your life empowers you to stay on top of preventive care, which is the cornerstone of lifelong oral health. Those regular check-ups and cleanings, often 100% covered, are what stop minor issues from turning into painful and expensive emergencies.

For instance, catching a small cavity early is a simple, affordable fix. But if you let it go, that same cavity could easily require a root canal and crown—procedures that are far more involved and costly. Your insurance acts as a safety net, making it easy and affordable to be proactive.

Understanding the details is just as important. As you look at different dental insurance san diego providers, you'll see a lot of options. You can dive deeper by checking out our detailed breakdown of affordable dental insurance plans to see how they compare.

What to Look For in a Plan

When you’re comparing plans, it's crucial to look beyond the monthly premium. That number is just one piece of the puzzle. Here are the key factors to focus on to make a smart decision:

- Network of Dentists: Is your favorite San Diego dentist on the list? PPO plans usually have large networks and let you go out-of-network, while DHMOs require you to stick to their specific list of dentists.

- Coverage for Major Procedures: Dig into how the plan handles bigger-ticket items like crowns, bridges, and implants. Look for waiting periods and find out what percentage they cover (the coinsurance).

- Annual Maximums and Deductibles: A low deductible is great because it means your insurance kicks in faster. A high annual maximum is also a huge plus, giving you more financial breathing room if you need significant work done in one year.

PPO vs. DHMO: Your Two Main Choices

When you start researching dental insurance here in San Diego, you’ll quickly see that most plans fall into two categories: PPO and DHMO. This is likely the biggest decision you'll make, as it impacts everything from which dentists you can see to how much you'll pay out-of-pocket.

At its core, the choice is a classic trade-off: Do you prefer more flexibility, or do you want more predictable costs?

Think of a PPO (Preferred Provider Organization) plan like having an all-access pass to your favorite restaurants. You’re free to visit almost any dentist you choose, including specialists like an orthodontist or oral surgeon, without needing a referral first. This freedom is a major advantage if you already have a dentist you trust or simply want the ability to choose your provider without restrictions.

A DHMO (Dental Health Maintenance Organization), on the other hand, is more like a curated dining club. You select a primary care dentist from a specific network, and they become your main point of contact for all your dental needs. If you need a specialist, your primary dentist will refer you to one within the same network. The trade-off for less choice is often a much lower monthly premium and a clear, fixed price for services.

A Closer Look at PPO Plans

There's a reason PPO plans are so popular—that flexibility is hard to beat. If being able to choose your own dentist or go directly to a specialist is important to you, a PPO is probably the right choice.

With a PPO, there’s a network of "preferred" dentists who have agreed to charge lower, pre-negotiated rates. Staying within this network ensures you get the most value. However, most PPO plans still provide some coverage if you go out-of-network; you’ll just pay more out-of-pocket since the insurance company will cover a smaller portion of the bill. It's an excellent model for families who need that flexibility and don't mind a slightly higher premium to get it.

Understanding the DHMO Model

DHMO plans are structured differently, with a focus on keeping costs down through managed care. Once you enroll, you select a primary care dentist from the plan's network who manages all your treatments. This structure helps keep care affordable for both you and the insurance company.

The financial upside is clear. DHMOs usually have very low deductibles (or none at all) and use a fixed copayment schedule. This means you know exactly what a filling or cleaning will cost before you even walk into the office, making it much easier to budget for dental care. For San Diegans who want to keep monthly costs low and are comfortable working within a set network, a DHMO is a fantastic, budget-friendly option.

PPO vs. DHMO Dental Plans At A Glance

To make the differences even clearer, let's break them down side-by-side. This table should help you quickly see which plan type aligns better with your priorities and budget.

| Feature | PPO (Preferred Provider Organization) | DHMO (Dental Health Maintenance Organization) |

|---|---|---|

| Dentist Choice | High flexibility; choose almost any dentist, in or out of network. | Must choose a primary dentist from the plan's specific network. |

| Referrals to Specialists | Not required. You can see a specialist directly. | Required. Your primary dentist must refer you to a specialist. |

| Monthly Premiums | Generally higher. | Generally lower, often significantly so. |

| Out-of-Pocket Costs | Varies; uses deductibles, coinsurance, and copayments. | Predictable; uses a fixed copayment schedule for services. |

| Out-of-Network Coverage | Yes, but at a higher cost to you. | Typically none, except for emergencies. |

| Best For | Individuals and families who value flexibility and want to keep their current dentist. | Individuals and families focused on budget-friendliness and predictable costs. |

Ultimately, there's no single "best" plan—only the one that's best for you.

Cost Differences in San Diego: A Real-World Example

The price difference between these two plan types can be significant. A great local example comes from the County of San Diego's dental insurance options for its employees.

Employees who choose a Delta Dental PPO plan pay a monthly premium of around $23.88 for an individual. In stark contrast, the DeltaCare USA DHMO plan is just $9.07 for individual coverage. That’s a massive difference in monthly cost. If you want to see the numbers for yourself, you can check out the 2025 Dental Comparison Flyer from CalHR.

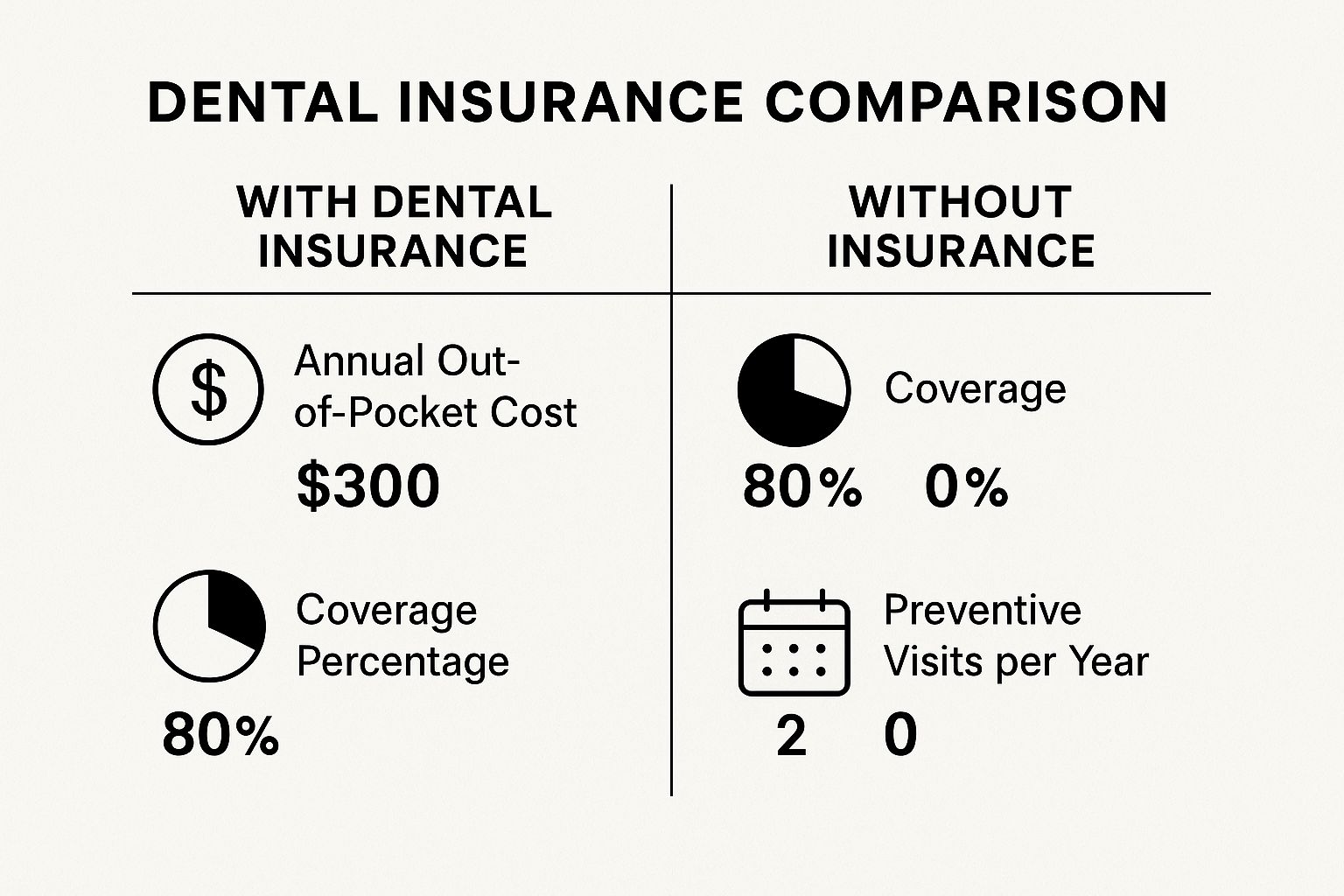

The image below highlights just how much of a financial impact having dental insurance can have on your annual costs and ability to get the care you need.

As you can see, a good plan doesn't just save you money; it encourages you to get the preventive care that keeps your smile healthy long-term. This is why staying on top of appointments for a professional dental cleaning is one of the smartest things you can do for your oral health.

Breaking Down the Costs of San Diego Dental Plans

To really understand the cost of dental insurance in San Diego, you have to look past the monthly bill. If you want to compare plans accurately and avoid surprise expenses, you need to speak the language of insurance. Let’s break down the key financial terms you’ll encounter.

Think of your dental plan's total cost as having four main components, with each one affecting what you pay out-of-pocket.

Your Monthly Premium

The premium is simply the fixed amount you pay each month to keep your insurance active. It's like a subscription fee for your dental coverage. You pay it whether you visit the dentist or not, just to maintain the plan.

What determines the price? A PPO plan, which offers more freedom to choose your dentist, will almost always have a higher premium than a more restrictive DHMO. Similarly, a plan that covers major work like crowns or implants will cost more per month than a basic plan focused only on preventive care.

The Annual Deductible

Next up is the deductible. This is the specific amount you have to pay for dental work yourself before your insurance company starts contributing. It’s like the initial hurdle you clear each year.

For instance, if your plan has a $50 deductible, you’ll cover the first $50 of your dental bills (usually for services beyond routine checkups). After you've met that amount, your insurance begins sharing the costs. The good news is most plans waive the deductible for preventive care like cleanings and exams to encourage you to stay on top of your oral health.

Copayments and Coinsurance

Once your deductible is met, you’ll start sharing the cost with your insurer. This usually happens in one of two ways:

- Copayment (Copay): This is a simple, flat fee you pay for a specific service. DHMO plans frequently use copays. You might pay a set $25 for a filling, and that’s it—very predictable.

- Coinsurance: This is a percentage of the total cost you're responsible for. PPO plans typically use this model. For example, your plan might cover 80% for a filling, which means you pay the remaining 20%.

Understanding this distinction is crucial, especially when planning for major procedures. Our guide on dental implant prices shows the kind of costs involved, which makes understanding your coinsurance percentage incredibly important for budgeting.

What San Diegans Can Expect to Pay

The price for dental insurance here in San Diego can vary widely. One market analysis of 44 different plans in California found that monthly premiums for a 33-year-old could be as low as $6.95 for a basic DHMO or as high as $93.65 for a top-tier PPO plan that also includes vision.

The average premium worked out to be $45.48 per month. You can see the full breakdown of your options in a comprehensive report about California dental insurance costs.

By getting a firm grip on these four parts—premium, deductible, copay, and coinsurance—you stop being a passive consumer and become an empowered patient. You can confidently compare what San Diego dental plans are truly offering and pick one that fits your budget and your health needs perfectly.

Once you understand these costs, the next step is to fit them into your overall financial plan. For some great tips on managing your money effectively, check out this guide on mastering budgeting for financial freedom. This helps ensure that taking care of your smile doesn't throw your financial well-being off track.

How to Choose and Enroll In Your Dental Plan

You've got the lay of the land on plan types and costs. Now for the most important part: enrolling in the right dental insurance for you and your family here in San Diego. The process is much more straightforward than it seems once you know where to look and what questions to ask.

There are three main ways people get dental coverage, and the best path for you usually depends on your employment and personal situation.

Three Paths to Dental Coverage

Let's break down the most common ways to get insured in San Diego.

Through Your Employer: For most people, this is the easiest and most affordable option. Companies often handle the research and typically subsidize a portion of your monthly premium. The only catch is that you usually have to sign up during a specific "open enrollment" period once a year.

On the Covered California Marketplace: If you're self-employed, a freelancer, or your job doesn't offer dental benefits, the state's health insurance marketplace is an excellent resource. It allows you to compare different plans side-by-side. Just like with employer plans, you'll need to enroll during the annual open enrollment window, which is typically in the fall.

Directly from an Insurance Provider: You can always go straight to the source and buy a plan from a carrier like Delta Dental, Anthem Blue Cross, or Cigna. This gives you the freedom to enroll whenever you want, but you'll likely pay more than you would for a group plan through an employer.

Your Pre-Enrollment Checklist

Before you commit to a plan, you need to play detective. Asking a few key questions upfront can save you significant headaches and money down the road.

Think of this as your essential checklist for vetting any dental insurance San Diego plan.

- Is my current dentist in-network? This is question number one for a reason. If you love your dentist, make sure they're in the plan's network to get the best rates.

- What are the waiting periods? This is a big one. Some plans make you wait six to twelve months before they'll cover major work like a crown or bridge. If you think you'll need a major procedure soon, you’ll want a plan with no waiting periods.

- What is the annual maximum? This is the cap on what your insurance will pay out in a year. If you anticipate needing a lot of dental work, look for a higher maximum—something like $2,000 or more is ideal.

- How does the plan cover preventive vs. major care? Good plans cover preventive care (cleanings, X-rays) at 100%. Then, check the coverage levels for everything else. Fillings are usually covered at 80%, while bigger jobs like root canals or crowns often get 50% coverage.

- Are orthodontics or cosmetic procedures included? Coverage for braces is tricky; it’s often sold as a separate add-on or isn't covered at all for adults. Purely cosmetic work like veneers is almost never covered, so always read the fine print.

A good decision isn't just about finding the cheapest monthly premium. It’s about choosing a plan with benefits you'll actually use—one that fits your real-life needs.

Of course, finding the right plan is only half the battle; you also need a great dentist. If you're looking for a new provider, our guide on how to find a new dentist when you are moving has some great advice to make the switch seamless. With this checklist in hand, you can confidently pick a plan that works for you.

Getting The Most Value From Your Dental Benefits

You've landed a good dental insurance San Diego plan. That's a huge win. But having the plan is one thing; knowing how to use it like a pro is something else entirely. Think of your dental benefits as a toolkit for keeping your smile healthy—if you know what each tool does, you can get the most value without wasting a cent.

The secret isn't complicated. It’s all about shifting from a reactive mindset ("my tooth hurts!") to a proactive one. Instead of waiting for a problem to arise, you can use your plan’s features to prevent issues before they even start. This simple change will save you significant money and discomfort down the road.

Embrace The Power Of Preventive Care

Believe it or not, the most valuable part of your dental plan is often the most underused: preventive care. Most PPO and DHMO plans will cover your routine cleanings, exams, and yearly X-rays at 80-100%, frequently before you even have to touch your deductible. This isn’t just a nice perk; it's the core of a smart oral health strategy.

Why is this so important? These check-ups are your first line of defense. During a routine exam, your dentist can spot a tiny cavity and fix it with a simple filling. If you skip that appointment, that same small cavity can quietly grow into a much bigger problem, eventually needing a root canal and a crown—a far more expensive and involved process.

Using your preventive benefits is like getting a regular oil change for your car. It’s a small, predictable investment that helps you avoid a massive, unexpected breakdown on the side of the highway.

Track Your Annual Maximum Wisely

Every dental insurance plan has an annual maximum. This is the absolute highest dollar amount your insurer will pay for your dental work within a plan year, typically somewhere between $1,500 and $2,500. Once you hit that limit, any other costs are 100% your responsibility until the plan renews.

A little strategic planning can help you avoid hitting that financial wall unexpectedly. Here’s how to stay on top of it:

- Know Your Number: At the start of your plan year, confirm exactly what your annual maximum is and track your usage.

- Phase Major Procedures: If you know you need extensive work, like a crown, bridge, or several fillings, have a conversation with your dentist. It’s often possible to phase the treatment, starting part of it toward the end of one plan year and finishing it after your benefits reset in the next.

- Don't Let It Go to Waste: Remember, your dental benefits don't roll over. If you have funds left in your plan toward the end of the year, it’s the perfect time to schedule any treatments you’ve been putting off.

Understand Coverage For Different Treatments

It's crucial to know how your insurance company categorizes different procedures, as this directly affects what you'll pay out-of-pocket.

- Restorative Care: This category includes treatments that fix a functional issue, like fillings for cavities or crowns for cracked teeth. These are usually covered at a high percentage, often 50-80%, after you’ve met your deductible.

- Cosmetic Dentistry: Procedures performed purely for aesthetic reasons—like teeth whitening or most veneers—are almost never covered by insurance. The exception? If a veneer or crown is deemed medically necessary to restore a damaged tooth, your plan might contribute.

The good news for San Diego residents is that the cost of dental plans has been fairly stable. The weighted average rate change is projected to be a modest 1.55%, making it easier to budget for your care. Plus, family dental plans can often be added for adults, and children under 19 typically get standard dental benefits included with their health plans. You can dig into the details by checking out these 2025 dental rate trends from Covered California.

In-Network vs. Out-of-Network: What It Means for Your Wallet

To get the most out of your dental insurance San Diego plan, one of the first things to understand is the difference between "in-network" and "out-of-network." This detail has a huge impact on your final bill and the simplicity of the process. Getting this right is the key to avoiding unexpected expenses.

Think of an in-network dentist as a trusted partner of your insurance company. They’ve signed a contract, agreeing to charge special, pre-negotiated rates for their services. When you see an in-network dentist, you benefit from these discounted prices, which can dramatically lower your out-of-pocket costs.

An out-of-network dentist, on the other hand, doesn't have that same agreement. While many PPO plans still allow you to see them, your insurance will cover a much smaller portion of the cost. You’re responsible for the difference between what the dentist charges and what your plan is willing to pay—a gap that can be significant.

The Easiest Way to Save Money? Stay In-Network.

Choosing an in-network dentist in San Diego is the single best move you can make to keep your dental bills manageable. The savings are built right into the system through those negotiated fees.

Let’s say a crown typically costs $1,500. An out-of-network dentist will charge you that full price. But an in-network dentist might have an agreement with your insurer to charge only $1,100 for the exact same procedure.

Your insurance then pays its share (let's say 50%) based on that lower, contracted rate. So not only do you get an immediate discount, but your final bill is calculated on a smaller number. As an added bonus, in-network dentists handle all the paperwork and claims for you, making your life much easier.

Visiting an in-network dentist is like having a VIP pass. You get exclusive pricing and streamlined service, ensuring you pay the lowest possible amount for top-notch care without any of the administrative headaches.

How to Check if Your San Diego Dentist is In-Network

Never just assume a dentist is in your network. Insurance networks can and do change, so it's always smart to double-check before scheduling an appointment. A few minutes of confirmation can easily save you hundreds of dollars.

Here’s a simple, three-step process to make sure:

- Use Your Insurer’s Website: The most reliable method is to log into your insurance provider's portal and use their "Find a Dentist" tool. You can search by name or location to pull up a current list of approved dentists.

- Call Your Insurance Company: Still not sure? Flip over your insurance card and call the member services number. A representative can look up a specific dentist and confirm their status with your exact plan.

- Ask the Dental Office Directly: Just give the clinic a call and ask, "Do you participate in the [Your Insurance Plan Name] network?" Be specific—for example, say "Delta Dental PPO," not just "Delta Dental"—because an office might be in-network with some plans from an insurer but not all of them.

By taking a moment to confirm your dentist's status, you put yourself in control of your costs and ensure your dental insurance San Diego plan is truly working for you.

Your Top Questions About San Diego Dental Insurance Answered

Let's be honest, dental insurance can be confusing. To cut through the clutter, we’ve put together straightforward answers to the questions we hear most often from our patients right here in San Diego. A little clarity goes a long way in helping you make confident choices about your dental care.

Does dental insurance in San Diego cover orthodontics?

This is a big one, and the short answer is: it depends entirely on your plan. Braces or clear aligners aren't automatically included in every policy.

Many comprehensive PPO plans offer some help with orthodontic costs. A common scenario is the plan covering 50% of your treatment, but only up to a lifetime cap—often around $1,500 to $2,500. On the flip side, more basic plans or DHMOs might not cover orthodontics at all, especially for adults.

Key Takeaway: Never assume your braces are covered. The best move is to check your plan's "Summary of Benefits" or call your insurance company directly to ask about your orthodontic clause before starting treatment.

Are cosmetic treatments like veneers covered?

Understanding this is crucial. As a rule of thumb, procedures that are done purely for aesthetic reasons, like professional teeth whitening or veneers meant only to enhance your smile, are not covered by dental insurance.

However, there can be a gray area. Sometimes, a procedure has both cosmetic and restorative benefits. For instance, if a veneer or crown is needed to fix a severely broken or chipped tooth, your insurance might cover part of the cost because it's restoring the tooth's function. Your dentist can submit a pre-treatment estimate to your insurer to see exactly what they'll cover.

What happens if my dental work exceeds my annual maximum?

Think of your annual maximum as a hard spending limit set by your insurance company for a single year. For most dental insurance San Diego plans, this cap usually falls somewhere between $1,000 and $2,000.

If your treatment costs go over that limit, you are responsible for 100% of the remaining balance. The good news is that your annual maximum resets when your plan year starts over. This is exactly why we work with patients to strategically plan major procedures, sometimes spreading them out across two plan years to make the most of your benefits.

Can I use two dental insurance plans at once?

You absolutely can! It’s called dual coverage, and it’s quite common when both partners in a family have dental benefits through work. Using both can be a fantastic way to lower your out-of-pocket costs for major treatments.

Here’s how it works: one plan acts as the "primary" and pays its share first. Then, the bill goes to the "secondary" plan, which may pick up some or all of the remaining cost, based on its own rules. It’s a great way to get more mileage out of your benefits.

Ready to make the most of your dental benefits with a team that puts your smile first? At Serena San Diego Dentist, we help you understand your coverage and achieve your oral health goals. Schedule your consultation today by visiting us at https://serenasandiegodentist.com.